Follower Size vs. Customer Affinity: Flat Across Tiers

Results as of

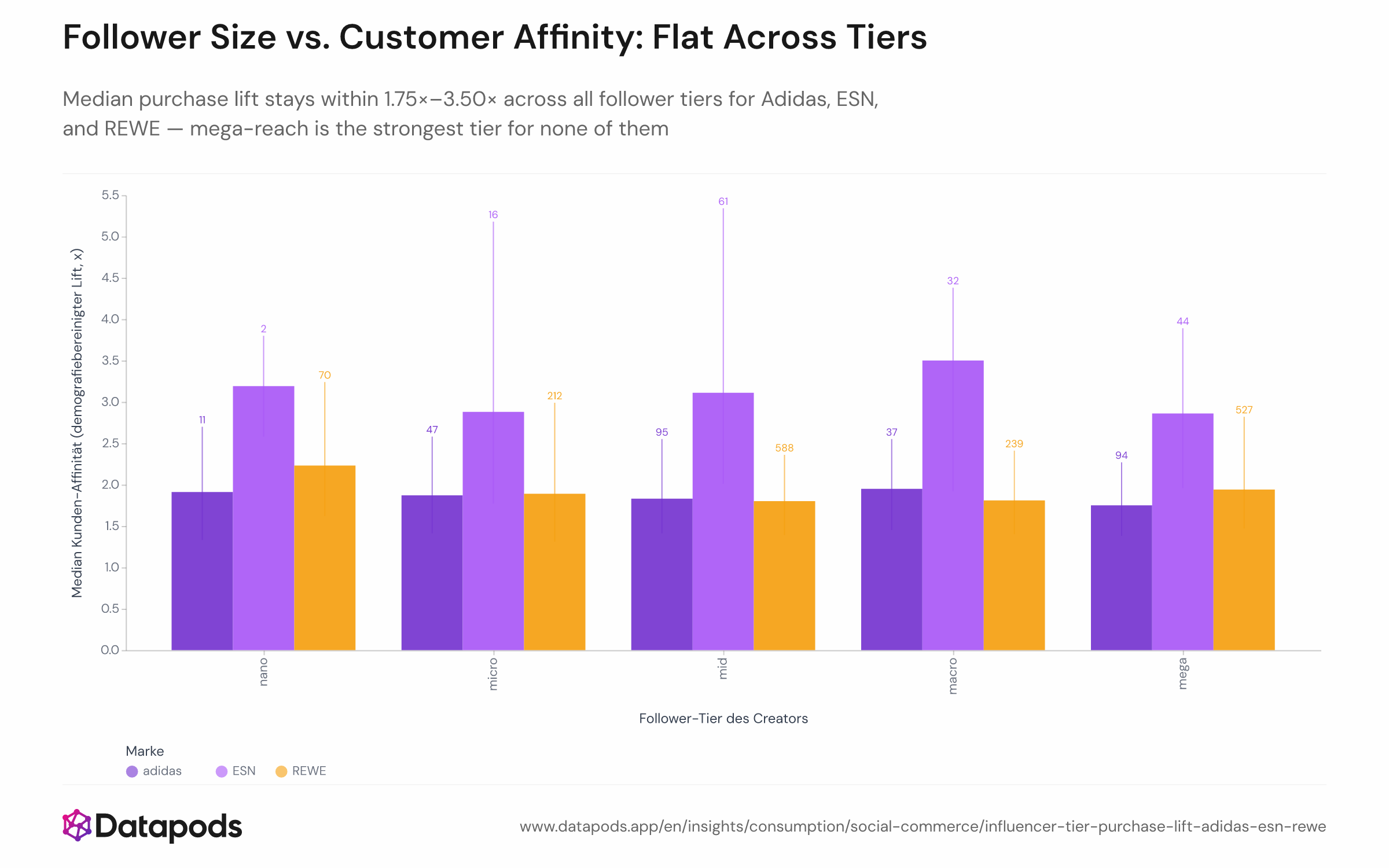

Review June 2025 – June 2026: Median purchase lift stays within 1.75×–3.50× across all follower tiers for Adidas, ESN, and REWE — mega-reach is the strongest tier for none of them

Info

- Sample size

- n = 3,876

- Data date

- June 2025 – June 2026

- Segment

- All segments

- Platform

- Browsing, Purchases

- Market

- Germany

Analysis

Across more than 3,800 creator candidates assessed for Adidas, ESN, and REWE, median purchase lift is remarkably stable from nano to mega tier — contradicting the widespread belief that smaller creators reliably out-convert their larger counterparts at the point of sale.

The nano-advantage narrative doesn't survive the full distribution

The industry consensus in 2025–2026 strongly favours nano and micro creators, pointing to engagement rates of 4–8% versus under 1% for mega accounts. But engagement and actual purchase conversion are different signals. When demographics-adjusted purchase lift is measured across the entire candidate pool — not cherry-picked examples — the tier gap shrinks to noise. For Adidas (nano–mega range: 1.75×–1.95×) and ESN (2.86×–3.50×), statistical testing confirms no significant tier effect. REWE shows a statistically detectable difference, but the spread (1.80×–2.23×) is small in commercial terms. The extreme individual lifts of 6×–12× sometimes cited for small creators are right-tail outliers, not the typical result in their segment. For brands negotiating creator fees, this means follower count alone is a weak proxy for expected audience affinity — creator-to-brand fit and audience overlap quality matter more than tier.

This analysis is based on public segment data. For deeper cuts, use our Enterprise interface.

Methodology

Purchase lift was measured for all creator candidates evaluated for Adidas, ESN, and REWE using a creator–audience affinity model that identifies creators whose followers over-index on actual brand purchases. Lift figures are demographics-adjusted (age × gender) based on 12-month purchase and follow behaviour among verified brand buyers. Each creator was assigned to a follower tier (nano, micro, mid, macro, mega) using a standardised classification. The chart shows median lift and the interquartile range per tier and brand; candidate counts per cell are indicated on the chart. The observation window covers June 2025 to June 2026.