Marketplace vs. Direct Retailer Browsing Share in Germany — Q1 2024–Q1 2026

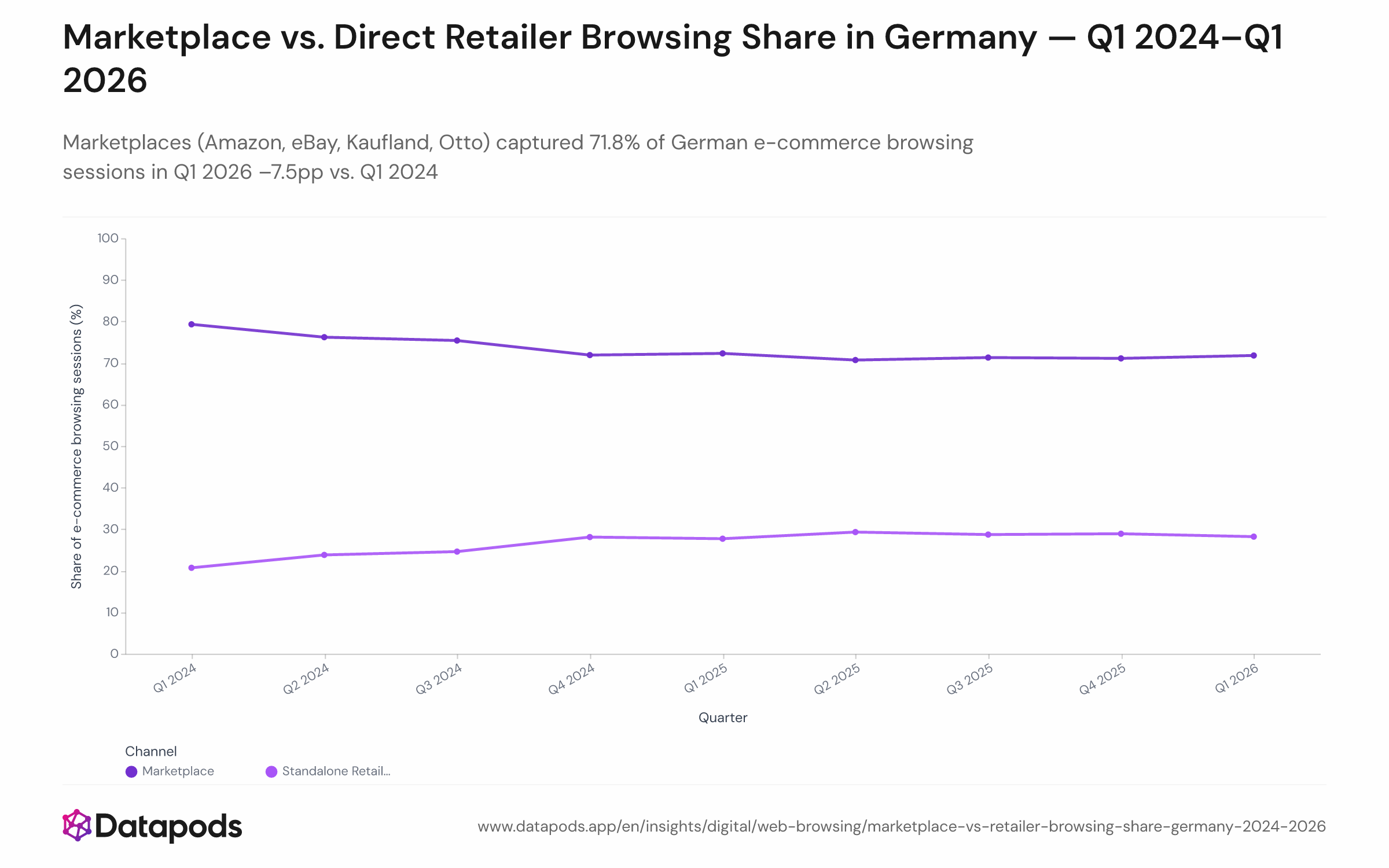

Review Q1 2024–Q1 2026: Marketplaces (Amazon, eBay, Kaufland, Otto) captured 71.8% of German e-commerce browsing sessions in Q1 2026 –7.5pp vs. Q1 2024

Info

- Data date

- Q1 2024–Q1 2026

- Segment

- All segments

- Platform

- Browsing

- Market

- Germany

Analysis

German e-commerce browsing in 2025 still orbits four platforms — amazon.de, ebay.de, kaufland.de, and otto.de — but their combined session share has fallen from a peak of 79.3% in Q1 2024 to a stable plateau of ~71–72% from Q4 2024 onward. That 7.5 percentage-point structural shift is the clearest sign yet that standalone retailers are reclaiming attention from shoppers who once defaulted to marketplace starting points.

Amazon's internal share slips as Kaufland and Otto gain ground

The rebalancing isn't uniform within the marketplace channel itself. Amazon's share of marketplace sessions fell from roughly 70% to 60.7% between Q1 2024 and Q1 2026, as kaufland.de and otto.de expanded their browsing footprints. This mirrors broader revenue data: the HDE Online Monitor 2026 reports that around 57% of total German online commerce ran through marketplaces in 2025, with marketplace revenue growing faster than the overall market — yet analysts at xpert.digital note that Amazon is expected to cede structural share for the first time in 2026, with Kaufland, Otto, and eBay absorbing the difference. The EU's abolition of the €150 duty-free import threshold effective July 2026 further strengthens domestic marketplace positions relative to Chinese cross-border platforms. For brands and merchants, a browsing share that has stabilised rather than collapsed suggests marketplaces remain indispensable discovery channels — but the era of near-80% concentration is over.

This analysis is based on public segment data. For deeper cuts, use our Enterprise interface.

Methodology

Session share is calculated as the proportion of e-commerce browsing sessions recorded at marketplace domains (amazon.de, ebay.de, kaufland.de, otto.de) out of all sessions at a defined universe of German e-commerce destinations. Data covers German online shoppers tracked across Q1 2024 through Q1 2026. The metric reflects within-period channel composition and is not a population reach projection. Early quarters in the window (Q1–Q2 2024) represent a smaller tracked user base; the panel expanded substantially through 2025.